How to Use Commodity Futures to Hedge?

Commodity futures are exchange-traded, standardised contracts that may be used to hedge against adverse future market positions. How to use commodity futures to hedge? That is what we aim to uncover in this article.?

What Is Hedging in Commodity Markets?

In the backdrop of commodity markets, hedging is a risk management strategy used by traders, producers, and consumers to safeguard against future price volatility and unfavourable price fluctuations. It serves as a form of financial insurance, enabling participants to lock in prices today for future transactions, thereby reducing uncertainty and safeguarding profit margins. The core objective of commodity hedging is risk management (reducing potential future losses) rather than speculation (earning profits).?

Adopting an offsetting and opposite position in the derivatives market (swaps, futures, and options) relative to a position held in the spot/physical market is the mechanism. The main hedging tools are primarily futures contracts (exchange-traded and standardised) and options (the right without the obligation to buy or sell).

What Are Commodity Futures?

Commodity futures are exchange-traded, standardised contracts that obligate buyers and sellers to purchase and deliver a particular quantity and quality of a raw material, such as oil, gold, or wheat. This has to be done at a set price on a future date. Hence, they are mainly used to hedge against price risks or to speculate on future price movements.?

Traded on exchanges such as the MCX, these futures contracts specify the quality, quantity, location, and delivery date, thereby eliminating the need for physical inspection of the goods. Traders only deposit a specific percentage of the contract value (the initial margin) rather than the full amount, thereby amplifying potential gains or losses.

Most contracts are netted/closed out before expiration, meaning they are cash-settled based on price differences rather than physical delivery. Contracts are marked to market on a daily basis, where the losses or gains are subtracted or added from the account margin.

The key participants are speculators or traders seeking to profit from price volatility without intending to take delivery, and hedgers (consumers or producers) who use futures to lock in prices and reduce risk.

The prices in this case are determined by current demand or supply levels and anticipations of future demand or supply. The types of commodities featured in these contracts include crude oil and other energy commodities, metals such as gold and iron ore, and agricultural commodities such as coffee and grains. Yet high leverage increases their risk and volatility, often leading to major losses.?

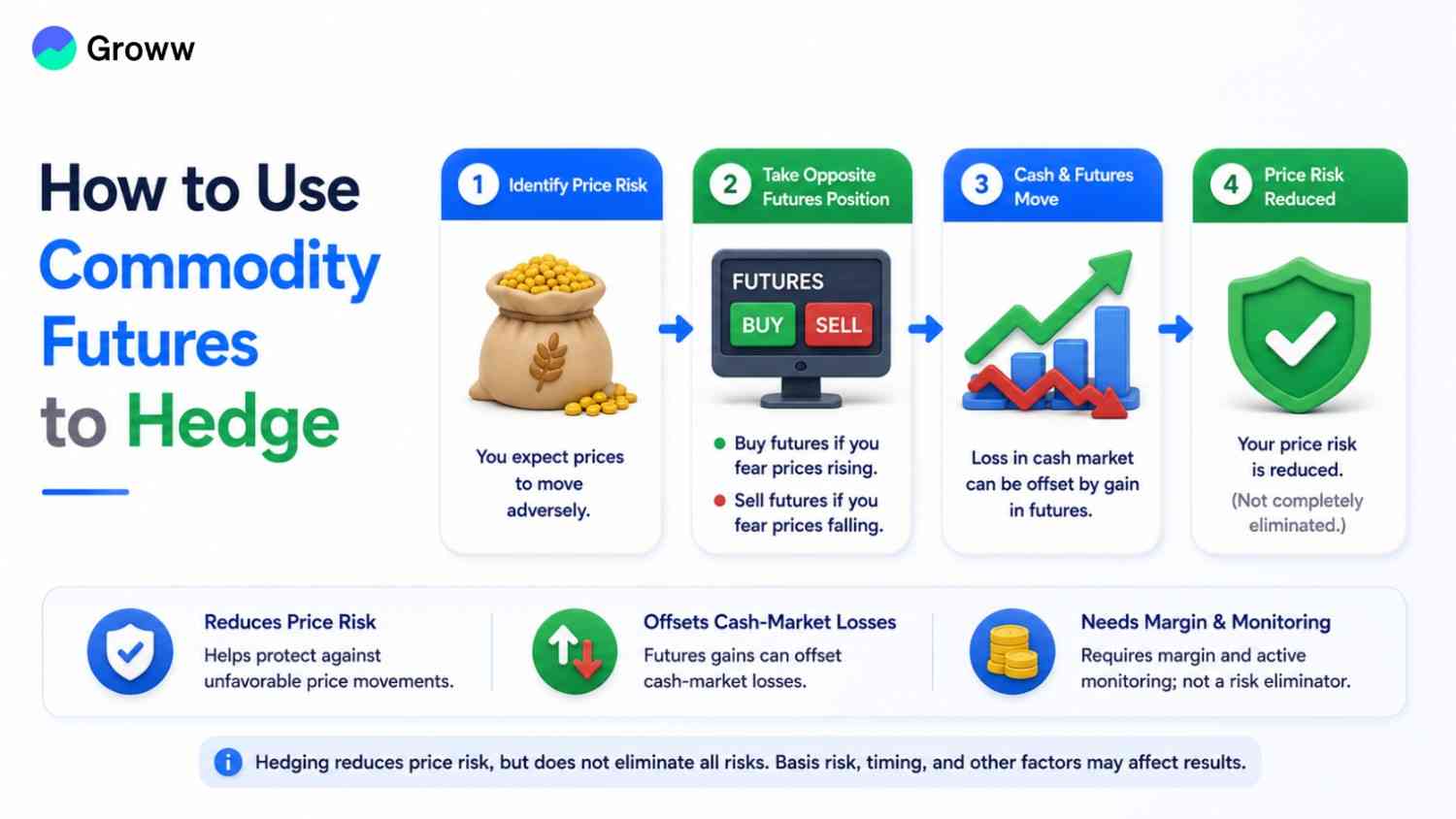

How Commodity Futures Help in Hedging

Commodity futures help with hedging by allowing consumers and producers to lock in prices today for later buying or selling, thereby mitigating price volatility risk. By adopting an opposite futures market position to their physical inventory, businesses often seek to secure their profit margins, stabilise costs, and safeguard against price fluctuations.?

This is how commodity futures enable hedging:?

- Locking in Prices: Producers (for example, farmers) may sell futures contracts to lock in a specific price for their product. This ensures guaranteed revenues irrespective of market dips. In the same manner, consumers (manufacturers, for example) may purchase futures to lock in their purchase costs.?

- Risk offsetting: This is an example of risk management using futures contracts. Participants may adopt a position in the futures markets that is completely opposite to their physical market positions. So, for example, if physical wheat is held by a farmer, he may short (sell) wheat futures. If the wheat price falls, the physical market loss will be offset by gains in the futures market.?

- Price volatility management: Hedging reduces exposure to sudden price spikes or even crashes caused by market uncertainties.?

By fixing output or input costs, businesses can create more accurate financial forecasts while reducing uncertainty. In this context, strategies such as short hedging (selling futures) by producers and long hedging (buying futures) by consumers are often seen in the market.??

Types of Commodity Hedgers

There are several types of commodity hedgers, including consumers, producers, and investors, who use derivatives, such as futures and options, to mitigate price risk. Let us look at these types in more detail below:?

- Producers (Short Hedgers): Mining companies, farmers, and oil producers are the main members of this category. They are the ones who face the risk that their product prices will fall in the future. Hence, they adopt a short futures position to lock in their selling prices.?

- Consumers (Long Hedgers): These are entities/consumers and manufacturers who depend on raw materials. So, an airline needs fuel, a food company requires grain, and a manufacturer may need metals. These companies often take long futures positions to hedge against rising costs.?

- FIIs and Institutional Investors: These are entities that use commodities to hedge against equity market volatility or inflation. Some may use oil or gold futures for offsetting portfolio risks.?

- Processors or Merchants: These are companies, such as refiners or grain elevators, that handle commodities between production and final consumption. They hedge to manage processing margins, not just price direction.?

Hedging Strategies Using Commodity Futures

There are highly strategic commodity hedging strategies that come into play with futures contracts. These include the following:?

Short Hedge (Producer Hedging)

A short hedge or seller's hedge is tailored to ensure protection against any decline in the prices of commodities that are presently owned by producers or those that will be produced in the future.

Commodity producers, inventory holders, miners, or farmers who intend to sell their products later usually use this strategy. Hence, they sell a futures contract at a pre-fixed price, thereby locking in the price today itself.

In case the spot price of the commodity falls before the sale, then the physical product’s loss will be offset by the gain on the short futures contract.?

Let’s take an example- suppose a farmer plants a crop in March, anticipating the harvest in September. Fearing the risk of falling prices, he sells September crop futures (short hedge). If the prices of the commodity come down by the harvest, the loss in the physical sale will be offset by the profit that he made with the short futures contract.?

Long Hedge (Consumer Hedging)

A buyer’s hedge or long hedge is designed to safeguard against any increases in prices of commodities that processors or consumers will have to buy in the future. This strategy is mainly used by processors, manufacturers, and retailers who need a steady supply of various raw materials. The consumer will purchase a futures contract, thereby locking in the purchase price today.?

So, in this case, if the commodity spot price rises before the actual purchase, the higher physical raw material cost will be offset by gains from the long futures contract.

To understand futures hedging in this context, suppose a chocolate manufacturer must purchase cocoa within the next 5-6 months. Fearing a rise in cocoa prices, the manufacturer will purchase cocoa futures (a long hedge) today.

If the price of cocoa rises exponentially in the spot market, the higher cost will be offset by the profit from the futures contract. Of course, there is always a basis risk, where the spot price and futures price do not always move in ideal correlation, thereby leading to an imperfect hedge.

At the same time, hedging also eliminates the possibility of benefiting from favourable price movements. Since futures are?marked to market daily, any sharp price movements against its?hedges may require the entity to deposit additional margin or cash.?

Step-by-Step Example of Hedging with Commodity Futures

Here is an example of how to use commodity futures to hedge against future uncertainty. This can be used to lock in a future price for any commodity, mitigating price risk.?

Here is a step-by-step short hedge example for producers.?

Suppose a trader anticipates a harvest of 1,000 kg of the commodity in September, currently priced at ?500/kg, and fears a price dip by the time of harvest.

In this case, the steps are the following:?

- Step 1: Risk identification (harvest value may come down)

- Step 2: The trader sells (shorts) 1,000 kg of the September commodity futures on the MCX at ?500/kg (total value of ?5,00,000)

- Step 3: The trader deposits a small margin upfront (5-10% of the total value) with the broker?

- Step 4: By September, the prices come down to ?400/kg. The trader?sells the commodity in the physical market at ?400/kg

- Step 5:? The trader then buys back (covers) the futures contract, thereby gaining ?100/kg in the futures markets after having lost ?100/kg in the physical market?

Here is a step-by-step example of a long hedge for consumers.?

Suppose a trader has to purchase 1 kg of gold in the next three months, but fears rising prices. In this case, the steps are the following:?

- Step 1: The trader identifies the risk of rising prices and purchases (goes long) 1 kg of gold futures for three months later at ?80,000/10g

- Step 2: Gold prices later rose to ?85,000/10g, after which the trader?then squares off or sells the futures contract at ?85,000/10g

- Step 3: While the trader paid ?5,000/10g more in the physical market, it gained the same amount through the futures contract by locking in the purchase price and avoiding the increase

Basis Risk and Its Impact on Hedging

It is now important to understand basis risk and its impact on hedging. This is essentially the financial risk that the price of any hedging instrument (such as futures contracts) and the underlying asset’s spot price do not move in perfect correlation. This leads to an imperfect hedge. The formula for calculation is the following -?

Basis = Spot Price - Futures Price

Such a risk may lead to sudden and unexpected losses or gains, thereby lowering the effectiveness of hedging. This involves mismatches in specific factors, such as the delivery point or location, timing, quality, and other aspects, between the hedging contract and the asset being held.

The key causes include supply and demand imbalances, transportation and storage costs, and other factors that may lead to unexpected basis fluctuations. Here are some types of mismatches worth knowing more about:?

- Locational: This is hedging at a different location than where the asset was originally sold or bought?

- Calendar: It is the mismatch between the date of the transaction and the futures contract expiration date?

- Quality/Product: This involves using a similar yet different asset for hedging (suppose jet fuel is used to hedge with crude oil futures)

Impact of the Basis Risk on Hedging:?

- Imperfect Hedging: The main impact is that the hedging instrument may not always perfectly offset spot market losses. This, in turn, leads to residual risks.?

- Unexpected Costs: A weakening (a faster fall in spot prices than in futures) or strengthening (a faster rise in spot prices than in futures) basis may create costs that make hedges less effective than expected.?

- Higher Volatility: While it is tailored to lower risk, a high basis risk may increase the volatility of the overall hedged position in some scenarios.?

Hedging vs Speculation - Key Differences

Here are the main differences between hedging and speculation that you should know more about. The two concepts are mainly different in their objectives. Let’s understand more about them below:?

- Goal: Hedging aims to lower risks and ensure stability, while speculation is aimed at maximising profits?

- Risk Tolerance: Speculators are more risk-oriented or aggressive, while hedgers are risk-averse or conservative by nature?

- Time Horizon: Hedging often comes with structural and long-term positions, while speculation is mostly for the short-term?

- Market Position: Hedgers usually adopt positions that are opposite to their existing exposure to offset risk. On the other hand, speculators usually take positions based on the anticipated movements in prices without any ownership of the underlying asset?

- Instruments: Both hedging and speculation use derivatives like futures and options with varying reasons (hedging is for protection, while speculation is mainly for leverage)

Benefits of Using Commodity Futures for Hedging

Here are some of the key advantages of hedging with commodity futures that you should know more about.?

- Mitigating price risks:

Hedging serves as insurance against adverse price movements. Producers or farmers may choose to lock in selling prices for future harvests. On the other hand, commodity consumers may lock in purchase prices for specific raw materials. This ensures they are safeguarded, irrespective of future market fluctuations.? - Budgeting and stable cash flows:

Through securing prices in advance, businesses may forecast revenues and costs more accurately. This ensures more predictable and stable cash flows, thereby enabling improved budgeting and long-term financial planning.? - Higher competitiveness and firm value:

Lowering price-volatility exposure will help firms avoid costs associated with financial distress, managerial risk aversion, and costly external financing. Hence, it considerably increases the firm's overall value, while the underlying stability also helps businesses offer more consistent customer pricing, thereby boosting overall market positioning and trust.? - Better inventory management:

Better hedging may help manage inventory-related risks, mainly caused by fluctuations in procurement prices. In some cases, it may also help lower the physical carrying cost of maintaining a large inventory by using futures positions.? - Access and liquidity:

Commodity futures markets typically offer greater liquidity, enabling market participants to enter or exit positions more easily. Contacts are standardised and traded on regulated exchanges, thereby reducing counterparty risk, increasing transparency, and enabling smoother transactions.? - Leverage/Capital Efficiency:

Futures contracts enable traders to control large positions with comparatively small margins or initial capital. This leverage makes hedging a good way to manage larger exposure without locking up considerable capital to hold inventory physically.? - Diversification and global market access:

Futures contracts enable higher exposure to the global commodity market, helping companies and investors diversify their portfolios while lowering dependence on conventional asset classes.? - Price discovery:

The interaction between sellers and buyers in the futures market shapes the collective anticipation of future commodity prices. Hence, all market participants, like consumers, policymakers, and producers, gain access to valuable information.?

Risks and Limitations of Hedging with Futures

There are various risks and limitations of hedging with commodity futures as well. These include the following:?

- Basis Risk:

The risk that the futures price does not move perfectly in sync with the spot price of the underlying asset. This mainly happens due to differences in quality, location, or even timing.? - Market and Liquidity Risks:

Illiquid contracts may make it harder to exit positions at fairer prices. Sudden price gaps in the market may render hedges ineffective.? - Leverage Risk and Margin Calls:

While futures safeguard against price declines, they require margin accounts. Any adverse movements may trigger margin calls, thereby necessitating more capital.? - Rollover Risk:

If a hedge is held beyond the contract's expiration, rolling over to a new contract may result in price discrepancies.? - Operational Risk:

It involves the complexities of timing, management, and implementation of the hedge, where there may be more errors than risk reduction.? - Limited Upside Potential:

Once a price is locked in, the hedger will miss out on potential profits if the market moves in their favour.? - Expenditure:

Transaction costs, including spreads and commission fees, may at times reduce or eliminate hedging benefits.? - Imperfect Hedge Risks:

Sometimes, there is no perfect correlation between the asset and the hedge, so some risk exposure remains.? - Complexity of Operations:

Hedging with futures requires advanced, up-to-date knowledge of market dynamics and movements. This makes it hard for beginners or inexperienced traders to implement these strategies.?

When Should You Use Commodity Futures for Hedging?

When is hedging with commodity futures more suitable? Here are some strategies and scenarios that are ideal in this regard.?

- Safeguarding against price declines:

The short/sell hedge technique is suitable for producers who fear a dip in the prices of the commodities they produce before they can sell.? - Security against price increases:

The long/buy hedge technique is ideal for processors, manufacturers, and consumers who must purchase raw materials and fear future price increases (before they can buy).? - Management of inflation or higher volatility:

You may use commodity futures to hedge against volatile market conditions during geopolitical upheavals or even high inflation. This ensures the stability of any business/entity.? - Standardised safety:

This is ideal when you have to hedge large and particular quantities of goods with the help of exchange-traded contracts.?

Of course, factors?such as?basis risk,?margin calls, and potential profit losses need to be kept in mind in this case.?

Common Mistakes in Commodity Hedging

There are some common mistakes in commodity hedging that you should avoid. They include the following:?

- Under or Over-Hedging: This involves mismatching the hedge volume with physical exposure, leading to higher costs or risks in turn.?

- Neglecting Basis Risk: You shouldn't ignore the possibility that local spot prices may not perfectly match futures contract prices.?

- Wrong Selection of Contracts: Selecting the wrong commodity type or maturity date (rollover risk) is another common mistake.?

- Adopting a Speculative Approach: You should never perceive the hedge as a form of speculation and try to outsmart or trick the market by timing entries instead of locking-in the known prices.?

- Neglecting Correlation and Volatility: You should never fail to account for rapid price changes and the asset's close relation to the hedge.?

- Lack of Formal Policies: Operating without clearly defined or pre-approved rules may lead to emotional, inconsistent, and ad hoc decision-making.?

- Forgetting about Cash Flow: Neglecting the impact of margin calls on overall liquidity and ignoring hedge accounting are other mistakes to avoid.?

Conclusion

As can be seen, hedging with commodity futures is a viable strategy for producers and consumers to protect against future price volatility. However, successful execution of the strategy requires advanced market knowledge and informed decision-making.?